AI Healthcare Trends 2026: Investments, Architectures, and the Next Wave of Clinical AI Tools

Slava Khristich

Vlad Nazarov

This article pulls together the most important 2026 AI trends in US healthcare: how adoption and spending accelerated in 2025, where AI is quietly becoming infrastructure, how platforms and providers are dividing responsibilities, and what that means for anyone planning products, budgets, or clinical roadmaps.

Artificial intelligence in healthcare has already been through its first real stress tests, and it held the line. Clinical pilots, production deployments, and regulatory reviews have shown that custom AI software solutions can reliably support doctors, nurses, and operations teams, which is why capital is now flowing in with far fewer caveats and carve-outs.

In 2025, the U.S. landscape is crowded with real systems, not just prototypes: ambient note-taking in exam rooms, AI triage in radiology, smart routing in call centers, and remote patient monitoring programs that actually change readmission curves. At the same time, most organizations are still wrestling with ungainly data stacks, fragmented workflows, and early attempts at governance boards and “AI formularies.” That tension between proven value and uneven execution is exactly what healthcare AI technology trends will need to resolve in 2026: fewer one-off experiments, more shared building blocks for data, models, safety, and monitoring across entire enterprises.

Looking ahead, 2026 is shaping up as the year where scale and discipline matter as much as raw innovation. The most interesting AI innovations in healthcare will likely be those that run safely across dozens of sites, wrap around everyday tools like EHRs and RPM platforms, and consistently move hard metrics such as throughput, access, and clinician well-being. In the sections that follow, we unpack how each major trend contributes to that shift, so you can read the signals, pressure-test your own plans, and spot the opportunities worth acting on next.

Why is TATEEDA qualified to tell you about healthcare AI trends in 2026?

TATEEDA is a custom healthcare software development company headquartered in San Diego, California. Since 2013, we have been building software for U.S. providers, payers, and healthtech firms, so our view of 2026 AI trends in US healthcare comes from real projects, not theory.

Over the years, we have worked with AYA Healthcare (a leading travel nurse staffing provider) and Abbott (a major biotech and medical device brand) as one of their software development partners. This gave us hands-on experience with how clinical staffing, operations, billing, and device data actually move through IT systems. Today, our teams:

- Build and integrate custom healthcare platforms for U.S. organizations.

- Connect EHRs, staffing, and billing systems to modern AI platforms for analytics, documentation, and decision support.

- Architect and implement AI agents that automate routine tasks in scheduling, credentialing, intake, and RCM.

- Design data flows that keep PHI inside compliant boundaries while still using advanced models and tooling.

This mix of engineering work and healthcare domain exposure is why we feel confident outlining AI innovations in healthcare 2026 and what they mean for teams planning their next generation of software.

Table of Contents

#1. 2025 Was the Breakaway → 2026 Will Be the Acceleration

By late 2025, the AI story in healthcare will have a clear shape in numbers: The global AI in healthcare market is estimated at about $39.25 billion for 2025, up from $29.01 billion in 2024, with analysts projecting a climb to $504.17 billion by 2032 at a roughly 44% CAGR. North America already holds just under 50% of that market, which means a significant share of this expansion will be written inside U.S. health systems, payers, and life sciences companies—exactly where 2026 AI trends in healthcare will be decided.

On the clinician side, 2024 marked an inflection point that 2025 has only accelerated. An AMA-backed survey found that 66% of U.S. physicians used AI in practice in 2024, up from 38% in 2023—a 78% jump in one year, with most usage clustered around documentation, coding support, discharge instructions, and translation. In parallel, an ONC data brief reports that 71% of U.S. hospitals were running at least one EHR-integrated predictive AI tool in 2024, up from 66% in 2023, signaling that predictive models are becoming standard infrastructure rather than experimental pilots. By 2026, it is reasonable to expect that these capabilities will be baked into default configurations of major EHRs and hospital platforms, not sold as optional extras—core to 2026 healthcare AI technology trends.

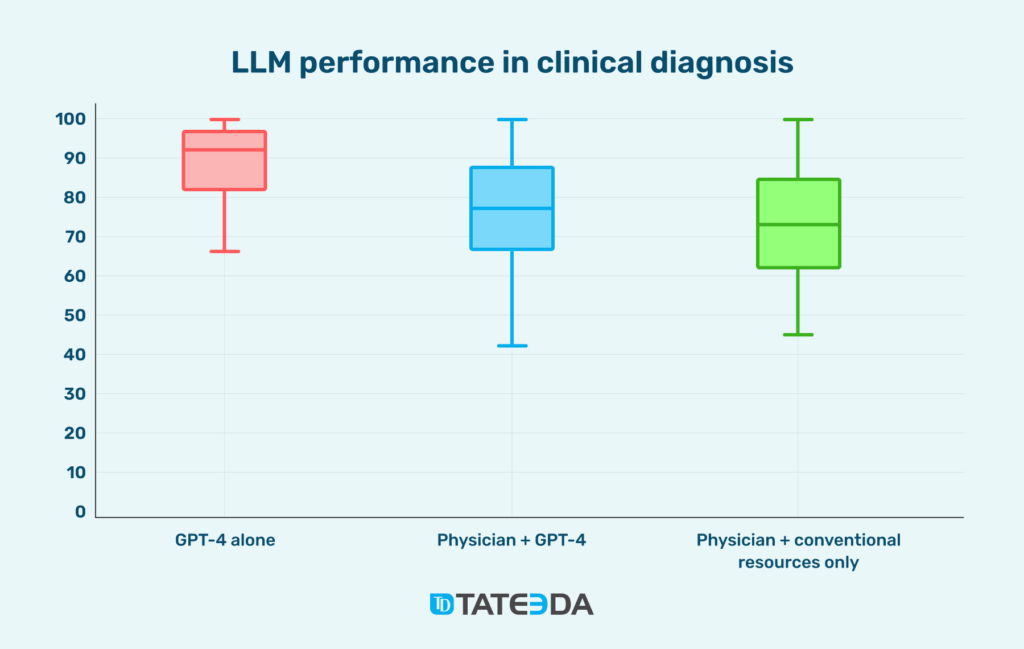

Clinical evidence is racing ahead alongside regulation. The 2025 Stanford AI Index highlights work by Goh et al. (2024) showing GPT-4 alone scoring higher and more consistently on complex diagnostic cases than physicians using either GPT-4 or conventional resources, hinting that carefully engineered human–AI teams may be the sweet spot rather than pure automation. We can assume that the latest late-2025 GPT-5 model can perform even better.

The same report notes that the FDA cleared 223 AI-enabled devices in 2023 versus six in 2015, and as sponsors move from narrow image classifiers to multi-modal, workflow-aware systems, they are effectively laying the groundwork for AI innovations in healthcare in 2026 that bundle sensors, LLMs, and decision support into unified, regulated products.

Zooming out to the macro AI economy, the same Stanford report notes that U.S. private AI investment reached $109.1 billion in 2024, with $33.9 billion globally flowing into generative AI alone, and 78% of organizations across sectors reporting AI use, up from 55% the year before. Healthcare is not separated from this tide; it is one of the most data-rich, high-stakes domains for that capital. For 2026 AI trends in US healthcare, the key shift is likely to be qualitative rather than merely quantitative—budget lines moving from isolated “innovation projects” into recurring operational spend, and evaluation frameworks evolving from “can it work?” to “does it measurably improve throughput, access, or outcomes at scale?”

Indicators that 2026 will build on 2025’s momentum:

| Indicator | 2023 baseline | 2024 reality | 2025 status / baseline for 2026 | 2026 direction (expert read) |

|---|---|---|---|---|

| Global AI in healthcare market size | n/a (earlier stage of current cycle) | $29.01B global market size | $39.25B projected for year-end 2025 | Trajectory implies mid-$50B range if the 44% CAGR holds, with North America keeping ~50% share |

| Physicians using AI in practice (U.S.) | 38% of physicians use AI | 66% use AI (mostly for documentation, coding, instructions) | Normalization of AI across both primary and specialty care | Likely to push into the 70–80% band, with more use in decision support and patient communication |

| Hospitals using EHR-integrated predictive AI (U.S.) | 66% report at least one predictive AI tool | 71% report such tools in production | Predictive models embedded in mainstream EHR deployments | Movement toward “AI by default” in core EHR releases; governance and monitoring become the new bottleneck |

| FDA-cleared AI/ML medical devices (cumulative) | Acceleration phase; sharp rise after 2019 | 223 AI-enabled devices approved in 2023 | 2025 pipeline skewing toward imaging, monitoring, and planning tools | More multi-modal, workflow-centric devices; AI becomes an expected feature of new imaging and monitoring hardware |

| Share of organizations using AI (all sectors, global) | 55% report using AI in 2023 | 78% report using AI in 2024 | Healthcare rides the same adoption wave as other industries | Procurement teams treat AI as a standard capability in 2026 RFPs, not a niche experiment, reinforcing 2026 AI trends in healthcare |

Learn more: ➡️ Vibe Coding vs. Professional Engineering: Is AI Making Development Services Obsolete?

#2. Pilots → Full-Scale Production: AI Becomes Healthcare Infrastructure (Once and Forever)

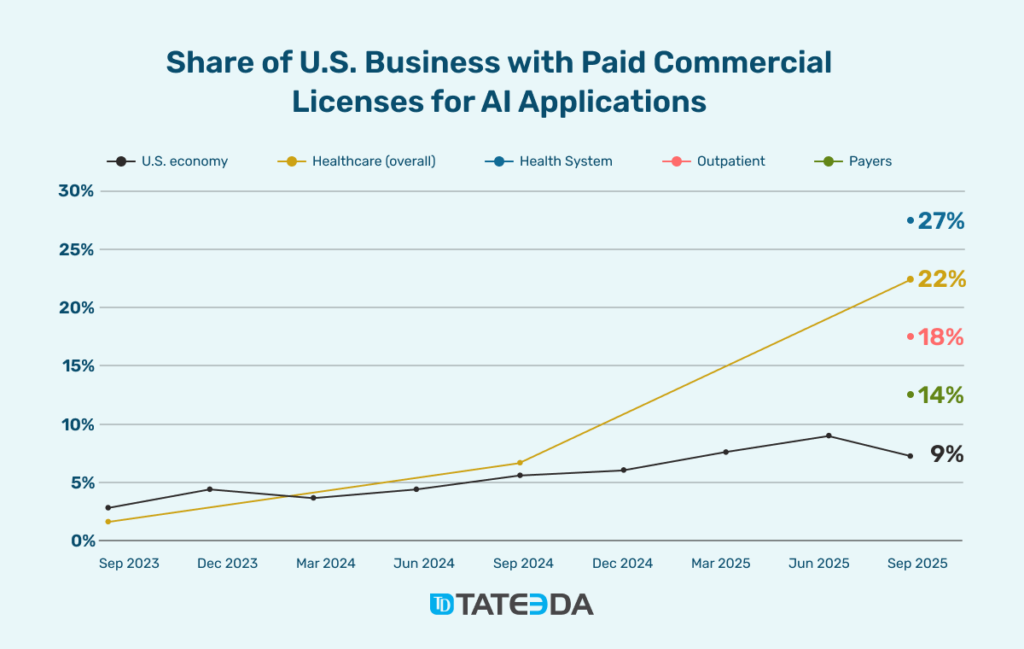

The U.S. healthcare sector has crossed a line that does not have a reverse gear. A few years ago, AI projects lived in isolated sandboxes and “innovation labs”; now they sit quietly behind everyday workflows, propping up scheduling, diagnostics, documentation, and billing all at once. According to the report 2025: The State of AI in Healthcare from Menlo Ventures, healthcare organizations are deploying commercial AI at roughly 2.2× the rate of the broader U.S. economy, with 22% of providers using domain-specific AI tools, up from just 3% two years back.

That shift shows up everywhere you look: ambient “scribes” wired into EHRs, radiology suites that lean on AI triage before a human ever opens the study, prior-auth and contact-center agents working in the background, even early generative models that explore drug candidates while researchers sleep. By the close of 2025, AI will no longer be an experiment at the edges of care; it will be part of the basic plumbing that 2026 AI trends in healthcare will simply assume is already in place.

#3. Clinician Shortages → Machine-Scale Support

None of this is happening in a relaxed environment. U.S. healthcare is a $4.9 trillion machine, roughly one-fifth of national GDP, that has historically spent far less on software and automation than its size would suggest, as the Menlo Ventures analysis points out.

Layer on chronic clinician shortages, post-pandemic exhaustion, revenue squeezed by admin overhead, and patients who have grown used to digital convenience in every other part of life, and you get a system that simply cannot push any harder on human effort alone. In that context, AI has started to look less like shiny gadgetry and more like extra hands.

“AI won’t magically solve clinician shortages, but it can radically change how scarce clinical attention is spent. The real step change comes when we stop using doctors as human APIs between systems and let software absorb everything that doesn’t require judgment or empathy.”

— Andrew G., Software Architect at TATEEDA

Ambient documentation tools peel hours of “pajama time” out of physicians’ evenings; imaging models pre-sort cases so radiologists can zero in on edge findings; workflow engines chew through prior auth, intake, and coding at machine speed so staff can focus on conversations instead of keystrokes. For anyone watching 2026 healthcare AI technology trends with a critical eye, this reclassification of AI from curiosity to workforce extension is the headline.

Large health systems are no longer flirting with the shift but budgeting for it: Mayo Clinic, for example, is mapping out more than $1 billion in AI investments across 200+ projects that touch both operations and direct patient care, a signal that the AI agenda now spans multiple planning cycles, not just a single pilot year.

#4. Capital Confidence = the Point of No Return

Financial markets spent 2025 making their own statement about where this is heading. Rock Health’s funding numbers, pulled together in a FierceHealthcare analysis, show U.S. digital health startups raising $6.4 billion in the first half of the year, up from $6.0 billion in H1 2024, with AI-enabled companies taking roughly 62% of that capital, about $3.95 billion in total.

Deal sizes for AI-focused startups ran 83% larger than their non-AI peers, and the biggest rounds clustered around platforms for documentation, clinical workflow orchestration, and data infrastructure. In parallel, the Menlo Ventures report estimates healthcare AI spending almost tripled to $1.4 billion in 2025, minting eight healthcare AI unicorns and a long tail of fast-growing companies in the $500M–$1B band.

For analysts sketching AI innovations in healthcare 2026 on the whiteboard, these numbers feel less like a spike and more like a new floor. With names like Hinge Health and Omada Health reopening the IPO window for scaled digital health players, 2025 looks less like a speculative episode and more like a structural reset; 2026 AI trends in US healthcare will be shaped less by whether providers try AI and more by how aggressively they scale what is already in production.

#5. Big AI Bets Quietly Affect the AI Industry Baseline for 2026

| Organization | Scale of AI initiative | Main AI focus areas | Expected / Reported impact | Notes |

|---|---|---|---|---|

| Kaiser Permanente | Deployment of Abridge’s ambient documentation across 40 hospitals and 600+ medical offices | Generative AI for clinical documentation; ambient scribing integrated into clinician workflow | Largest generative AI rollout in healthcare history; fastest technology implementation for Kaiser in 20+ years | Sets a new benchmark for system-wide rollout speed and scope for AI in clinical settings |

| Advocate Health | Evaluated 225+ AI solutions; selected 40 use cases for go-live | Microsoft Dragon Copilot for clinical documentation; imaging tools (Aidoc, Rad AI); AI for call centers, prior authorizations, referrals, and coding | Projected >50% reduction in documentation time; automation of prior auth, referral handling, and coding workflows | Shows how a multi-vendor AI portfolio can hit both clinical and administrative workloads at once |

| Mayo Clinic | Committing $1B+ in AI investment over the next few years across 200+ projects | Beyond admin automation, diagnostics, direct patient care, and clinical decision support | Long-term transformation program rather than isolated pilots; AI embedded in core clinical strategy | Positions Mayo as a reference point for large-scale AI roadmaps that blend operations and frontline care |

| SimonMed | Beyond admin automation, diagnostics; direct patient care; clinical decision support | Intake automation; ambient scribing for radiology; AI-driven revenue cycle management | Broad experimentation and scaling across the imaging pipeline; improved throughput and financial operations | Illustrates how independent radiology groups can act as fast adopters and integrators of diverse AI tools |

| Grow Therapy | Company-wide push to build an AI care companion across its digital mental health platform | Continuous AI support between therapy sessions; voice and language analysis for outcomes tracking | Moves from static questionnaires like PHQ-9 and GAD-7 to continuous, AI-based measurement; tighter feedback loops for therapists and patients | Early signal of how AI can reshape mental health care models with 24/7 support and dynamic assessment |

#6. AI in the Clinic: 2025 Benchmarks and the 2026 Upgrade Path

Ambient documentation as healthcare’s first real copilot

Ambient “AI scribes” are the clearest place where 2025 AI is already earning its keep. Comparative tests show that modern platforms such as Nuance DAX, Abridge, and others consistently save clinicians 1–2 hours of documentation time per day, while preserving note quality and coding detail; a Washington Post analysis of ambient AI in healthcare cites studies reporting roughly 20% cuts in note-taking time and 30% reductions in after-hours work. A multicenter JAMA Network Open study on ambient AI scribes found a 31% drop in reported burnout and a 30% boost in physician well-being, exactly the kind of outcome CIOs weigh when deciding which 2026 AI trends in US healthcare deserve recurring budget.

By 2026, the frontier will shift from “write the note for me” to “help me think better while I’m in the room.” Commentators already argue that the biggest value of scribes may lie in how they influence clinical decisions, not just how they document them, as highlighted in recent coverage of ambient AI’s impact on physician burnout and workflow. As 2026 healthcare AI technology trends mature, the most advanced deployments are likely to add:

- pre-visit chart summarization with flagged gaps or risks,

- in-visit prompts that surface guidelines or drug–drug interactions in context,

- post-visit automation that turns the same encounter into orders, letters, education, and billing artifacts.

In other words, ambient AI becomes the shell around the visit, not just the stenographer inside it.

Imaging and diagnostics: from second reader to traffic controller

On the diagnostics side, AI is quietly turning into the default “second reader.” The FDA now tracks more than 1,300 authorized AI-enabled devices on its AI-Enabled Medical Device List, with radiology accounting for the majority; a recent Biomedicines analysis of 2024 AI/ML device authorizations underscores how quickly that pipeline is accelerating. Reader-study and real-world data explain why: AI support in mammography can cut reading time by up to 90% while maintaining or improving accuracy, and a large Swedish trial reported 17.6% higher cancer detection with AI-supported screening in routine practice, as detailed in Nature Medicine and follow-on coverage of European AI breast-screening programs.

By 2026, AI innovations in healthcare 2026 are likely to push imaging tools beyond “spot the lesion” into orchestrating the whole diagnostic journey. Vendors are already bundling triage, worklist prioritization, structured reporting, and follow-up tracking into unified AI layers, while regulators respond with tighter expectations for evidence and lifecycle monitoring, as outlined in a recent FDA perspective on AI regulation in health care. Expect 2026 AI trends in healthcare to focus on which imaging platforms can prove real-world safety and impact at scale, not just publish striking AUC curves.

Remote monitoring and LLM copilots between visits

Outside the hospital walls, AI-driven remote patient monitoring (RPM) is where “AI at its best” already looks like fewer hospital beds filled. Virtual-ward pilots for heart failure and COPD that combine home sensors, predictive algorithms, and nurse outreach often report 20–25% reductions in 30-day readmissions, a pattern reinforced by a 2025 European Journal of Heart Failure meta-analysis on RPM. At UMass Memorial Health, a congestive heart failure program using Brook Health’s AI-driven platform cut 30-day readmissions by 50%, as reported in both AJMC and the system’s own program results release. For care managers planning 2026 AI trends in US healthcare, this is the pattern to watch: AI does not replace human outreach, it tells teams who to call today and why.

Large language models are starting to fill in the cognitive gaps around these data streams. A randomized trial in JAMA Network Open found that GPT-4 alone outperformed physicians using conventional resources on complex diagnostic vignettes, while also mapping out how doctor–LLM collaboration might evolve, as detailed in the study on the influence of GPT-4 on diagnostic reasoning. In parallel, stroke and rehabilitation researchers have shown that LLMs like ChatGPT-4 can deliver credible home-based education and coaching, with early evidence summarized in a recent comparative study of LLMs for stroke rehab education and a broader review of ChatGPT’s role in rehabilitation medicine. Looking ahead, 2026 AI trends in healthcare will likely focus on coupling LLM “explainers” with RPM and EHR data: summarizing last month’s sensor readings, drafting patient-friendly coaching scripts, and giving clinicians a faster way to see the story behind thousands of data points.

| Clinical domain | 2025 AI at its best (examples) | What changes by 2026 if trends continue? | Strategic takeaway for builders and buyers |

|---|---|---|---|

| Ambient documentation & workflow | AI scribes save 1–2 hours per clinician per day; 20–30% less note time and after-hours work; lower burnout. | From simple note generation to full visit choreography: chart prep, in-visit prompts, post-visit orders and letters. | Treat ambient tech as the main UX layer for clinical work. |

| Imaging & diagnostics | ~1,000 AI/ML devices in use, mostly radiology; faster reads and higher cancer detection in screening. | Standalone CAD tools become multi-step diagnostic copilots that triage, prioritize, and track follow-up. | Focus on real-world outcome gains, not just better test metrics. |

| Remote monitoring & chronic care | AI-guided RPM for HF/COPD cuts readmissions by 20–50% in leading programs. | RPM data streams fused with AI that flags risk, ranks outreach, and personalizes education. | Chronic-care economics become a key proving ground for AI in 2026. |

| LLM-based clinical reasoning & education | GPT-4-level models match or exceed physicians on hard diagnostic vignettes; support rehab and patient education. | Safer, clinic-tuned LLMs embedded in EHRs, RPM platforms, and patient apps with strong guardrails. | LLMs shift from side-channel chatbots to embedded clinical copilots. |

#7. Corporate AI Ownership Trends → Platforms, Data, and Deals in 2026 Healthcare

The headline story behind 2026 AI trends in healthcare is that no single group “owns” the space. Instead, big tech, incumbent healthcare vendors, and highly specialized startups have carved out complementary layers of the stack. Microsoft, Google, and Amazon concentrate on platforms and foundation models: Microsoft’s Nuance acquisition and Epic partnership on Azure OpenAI and DAX Copilot ambient tools are pushing GPT-4-powered clinical workflows into hospitals, Google’s Med-PaLM 2 medical large language model and Isomorphic Labs sit at the medical LLM and drug-design layer, while Amazon One Medical’s AI tools built on AWS Bedrock and HealthScribe tie analytics, transcription, and virtual agents into new care models. They provide the horsepower and generic tooling, but rarely define the full clinical experience alone.

“The question isn’t who owns healthcare AI, but who orchestrates data, models, and workflows into something clinicians actually trust and use. Over the next few years, the winners will be teams that treat Microsoft, Google, and Amazon as interchangeable utilities while they invest most of their energy into domain expertise, integration, and safety.”

— Slava K., CEO at TATEEDA

On top of these platforms, established healthcare vendors are rebuilding their product lines to reflect 2026 healthcare AI technology trends instead of “bolt-on” features. EHR providers such as Epic, Oracle Health, and athenahealth now ship native AI for voice-first note entry, predictive alerts, and coding suggestions to keep customers inside their ecosystems, often using the same underlying LLM infrastructure highlighted above.

Device makers like GE HealthCare, Siemens Healthineers, and Philips embed AI directly into scanners, monitors, and remote patient-monitoring hardware, supported by targeted deals such as GE HealthCare’s planned acquisition of Intelerad to create a more integrated imaging and AI workflow platform. Reuters Medtech and pharma collaborations, such as Danaher’s precision-diagnostics partnership with AstraZeneca, show how diagnostics and therapeutics teams increasingly co-own AI pipelines from biomarker discovery to treatment choice.

The third force shaping 2026 AI trends in US healthcare is the startup and growth-stage cohort that fills in the “last mile.” Hospital-facing tools like Viz.ai, Aidoc, RadNet’s Aidence, and Tempus specialize in acute pathways and oncology decision support; Hippocratic AI and Glass Health work on clinically tuned LLMs for physicians; Wysa and Cass experiment with AI-supported mental health; and Biofourmis, Current Health, AKASA, Olive, and Cedar tackle remote monitoring and revenue cycle automation.

Many of these companies engage in dual roles: direct sales to providers and white-label partnerships with big tech or payers such as Optum and CVS. M&A deals like Optum’s acquisition of Change Healthcare and New Mountain Capital’s roll-up of RCM vendors into “Smarter Tech” suggest that the next consolidation wave will focus on stitching these point solutions into broader AI operating layers.

How Different Players Shape the Healthcare AI Stack by 2026

| Segment | Representative examples | Primary AI role by 2026 | Typical value to providers | Position in AI stack / risk trade-off |

|---|---|---|---|---|

| Big tech platforms | Microsoft, Google, Amazon | Cloud AI platforms, LLMs, speech and vision services | Scalable infrastructure, reusable AI building blocks | High platform dependency; strong performance, but lock-in and pricing power |

| EHR vendors & clinical systems | Epic, Oracle Health, athenahealth, InterSystems | Native AI for notes, alerts, coding, workflow automations | “In-EHR” experiences with minimal workflow friction | Tight integration; limited flexibility if their AI roadmap lags |

| Medtech & diagnostics OEMs | GE HealthCare, Siemens Healthineers, Philips, Danaher | AI-enhanced imaging, monitoring, and diagnostic pipelines | Higher diagnostic throughput and accuracy | Device-embedded AI; upgrades often tied to hardware refresh cycles |

| Pharma & biotech collaborators | Pfizer–Tempus, J&J–BenevolentAI, GSK–Insilico, AstraZeneca–Danaher | AI for target discovery, trial design, and companion diagnostics | Earlier therapy options and smarter trial participation | Data access often gated by research agreements; long time horizons |

| Payers & RCM-focused players | Optum, CVS Health, AKASA, Cedar, “Smarter Tech” | Claims analytics, prior auth automation, billing AI | Fewer denials, cleaner revenue cycle | Strong influence on reimbursement rules; provider data flows back to payers |

| Clinical and RPM startups | Viz.ai, Aidoc, Aidence, Biofourmis, Current Health | Triage, remote monitoring, pathway-specific decision tools | Faster interventions, reduced readmissions | Narrow but deep; integration burden sits with the provider or integrator |

| Mental health & medical LLM startups | Wysa, Cass, Hippocratic AI, Glass Health | AI companions, clinician copilots, training and education | Extended support between visits, clinician education | Position in AI stack/risk trade-off |

#8. Health Tech Startups to Watch in 2026

1. Abridge

Abridge works on ambient clinical documentation: it listens to doctor-patient conversations and turns them into notes and related records that fit into hospital and clinic workflows. In 2025, Reuters reported a $250 million raise, while the company said its tools had already reached 100+ U.S. health systems and were on track to support 50 million conversations that year. What makes Abridge worth watching is that it has moved beyond simple note capture into the messier administrative side of care, where documentation, coding, and revenue questions overlap.

2. Nolla Health

Nolla Health sits closer to the consumer side of care, offering AI-supported skin assessment with physician review for acne treatment in the U.S., while its mole and skin cancer product remains more established in Norway for now. The company said it entered the U.S. after a $4.5 million seed round, had already treated 50,000+ patients in Norway in six months, and had expanded into 40+ U.S. states; Apple’s U.S. App Store also shows the Nolla Acne app at about 4.9 stars from 5.2K ratings. The interesting part is the structure: instead of stopping at detection or education, it folds assessment, clinician oversight, prescription access, and follow-up into one fairly compact care flow.

3. Ambience Healthcare

Ambience Healthcare builds AI tools for clinical documentation, coding support, and workflow assistance across several care settings, including places where the work is more chaotic than a routine outpatient visit. In mid-2025, the company announced a $243 million Series C at a $1.25 billion valuation, and Houston Methodist later reported figures including 80% utilization, a 40% drop in documentation time, a 33% reduction in after-hours work, and a 27% increase in patient face time. That matters because Ambience is not confined to the familiar “ambient scribe” category; it is trying to operate where inpatient complexity, coding logic, and clinical documentation all collide.

4. Tennr

Tennr is focused on a part of healthcare that patients rarely see clearly but often feel the effects of: referrals, intake packets, benefits checks, and the paperwork maze that comes before treatment even begins. Reuters reported that the company raised $37 million in Series B funding in 2024 at a valuation estimated between $200 million and $250 million, and Tennr says its system now handles 10+ million documents per month, drawing on 100 million medical documents, 2.3 billion data fields, and 8,000 criteria sets. Its appeal is fairly simple: rather than chasing flashy front-end medicine, it goes after one of the least glamorous choke points in U.S. healthcare, where delays and drop-offs happen every day.

5. OpenEvidence

OpenEvidence is building an AI medical search and reference tool for physicians who need fast access to published evidence, guidelines, and clinically grounded answers while making decisions. Reuters reported in January 2026 that it raised $250 million at a $12 billion valuation, with total funding nearing $700 million; Reuters also said the platform was used daily by more than 40% of U.S. physicians across 10,000+ hospitals and medical centers, supporting about 18 million consultations in December 2025 alone. What gives it a distinct profile is its narrower discipline: instead of trying to be a general-purpose AI assistant, it is positioning itself as a physician-facing evidence layer built around trusted medical sources.

The Final Word: Let TATEEDA Help You Navigate AI Trends

Put simply, 2025 showed that AI can safely pull real weight in U.S. healthcare; 2026 will be about scaling the winners and wiring them into everyday care, staffing, billing, and remote monitoring. The organizations that treat AI as part of their core infrastructure—not as a side experiment—will set the pace for the next few years.

TATEEDA is among the top AI development providers in San Diego, and we build real systems around these trends: AI copilots for clinicians, pharma and biotech data platforms, billing and RCM automation, patient CRM and engagement tools, and medical staffing and credentialing solutions. If you are planning your next healthcare AI project, this article is your map; the next step is deciding which of these ideas you want to turn into working software.